Euronext: Wide Moat At A 20% Discount

Euronext: Wide Moat At A 20% Discount

Euronext plays a crucial role in facilitating access to capital markets for companies and investors. This wide moat business is a backbone of my portfolio. Continue reading to find out why.

Welcome to Compound & Fire! We search for businesses which create strong shareholder value over time in order to get financial independence and retire early. Join for free if you haven’t subscribed yet.

Business overview

Euronext is a pan-European market infrastructure group operating:

Regulated and transparent equity and derivatives markets

One of Europe’s leading electronic fixed income trading markets

FX and power trading markets

The stock markets of Amsterdam, Brussel, Dublin, Oslo, Lisbon, Paris and Milan are all owned by Euronext. This makes them one of the largest centers for debt and funds listings in the world. Euronext also provides advanced market data services and a range of indices and index solutions, post trade infrastructures as well as innovative corporate and investors services.

Each participant on a stock exchange commits voluntary to place all their orders to buy or sell securities on a stock exchange. This gives Euronext a strong moat, as the monopoly ensures that all official market participants carry out all their security trading via a stock exchange.

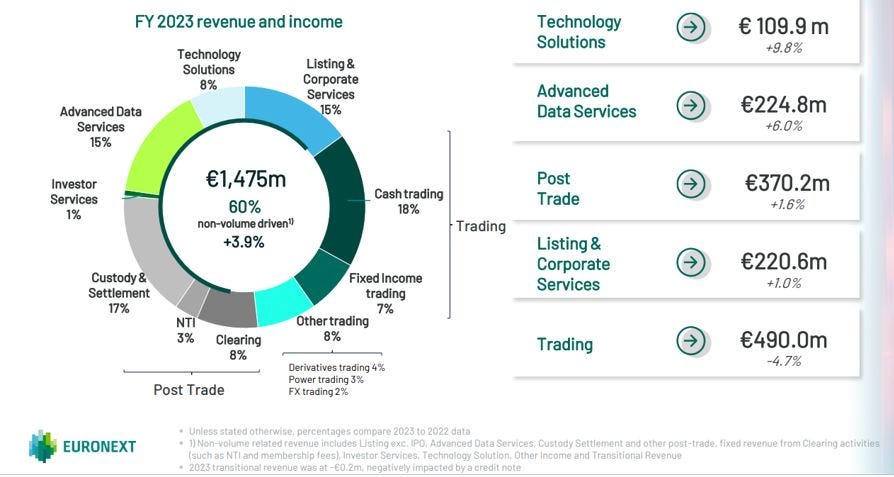

Euronext’s revenue by segment is shown below. Important note is the non-volume driven share, which is 60% of the total revenue.

Source: Euronext Q4 2023 Results - Presentation

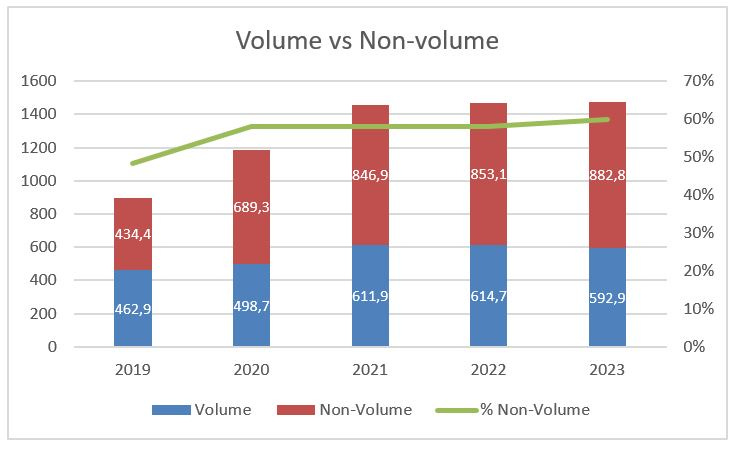

Euronext's non-volume related revenue has consistently grown as a percentage of total revenue, from 48.4% in 2019 to 60.0% in 2023, driven by acquisitions and organic growth in areas like Technology Solutions, Advanced Data Services, and Custody & Settlement:

If we look at the volume related revenue, then it’s good to be aware that in 2022, especially the first half year, there have been huge volatility spikes resulting in a high revenue for the volume related business In 2022. As a result 2023 has a tough comparison period and a lower volatility and lower trading volumes resulted in a decline in revenue. In 2023 non-volume related revenue covered over 140% of Euronext's underlying operating expenses excluding D&A.

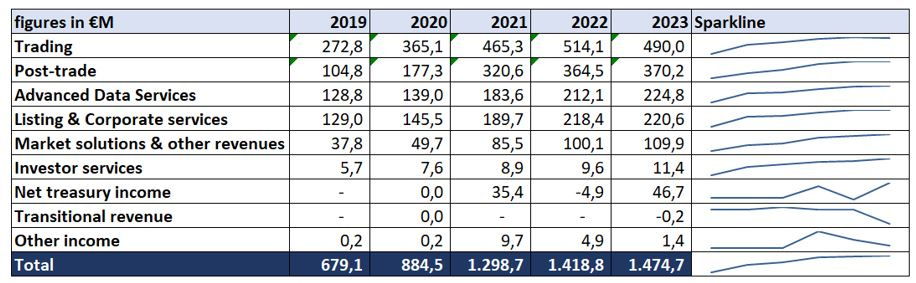

Now let’s have a closer look at the different market segments. The graph below shows the trend and sparkline for the different segments. The first six segments are growing overtime, except for Trading, which is volume related.

The 5-year revenue CAGR has been 19%, this includes M&A. In these years the net profit margin always has been above 30%. I would like to focus on the top four segments, as these cover 88% of the total revenue in 2023.

Trading

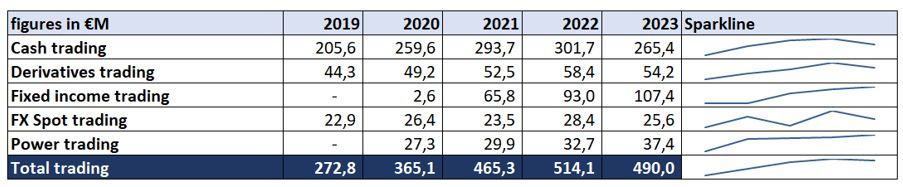

The trading segment consists of five sub-segments:

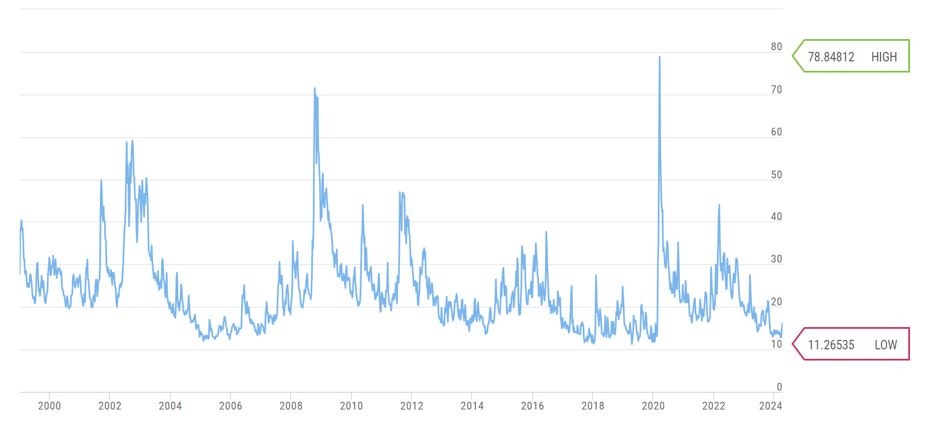

Total trading revenue was increasing from 2019 till 2022, but started decreasing in 2023. Highest decline is in Cash trading, which reflects a low volatility environment for equity trading. 2024 this low volatility in Q1 continued with a further 9% decline.

Source: Euro Stoxx 50 Volatility index from qontigo.com

As shown 2023 and the begint of 2024 are characterized by a very low average volatility. However, even with the low volatility in 2023, the revenue in 2023 is higher versus the high volatile 2020. This is the result of M&A. It’s important to verify whether Euronext is not losing market share in cash trading. Euronext wants to maintain a market share which is greater than 63%. In 2023 the average market share came in at 65.1% and I am confident they can manage to stay above 63% because of their moat. Because of the impact of the volatility, Euronext is a bit of a hedge when markets are more volatile.

Second largest subsegment is fixed income trading. This segment is made up of two parts: MTS, which is wholesale trading, and retail.

About MTS Euronext highlights in their annual report 2023:

“Since April 2021, Euronext is the majority owner of MTS S.p.A. (63,1%), the leading fixed income trading platform in Europe, number one for Dealer-to-Dealer (D2D) European Government bonds trading, number one in Italian repo trading and number three in Europe in Dealer-to-Client (D2C) European Government bonds trading. Euronext will strengthen its leading position in D2D, through an extended geographical reach and an expanded offering with new services. Its buy-side reach will be expanded through MTS BondVision together with the deployment of an added-value data offering. MTS will expand across the full value chain, by exploring opportunities to deploy new and existing solutions to meet the needs of its clients. In November 2023, MTS has launched MTS EU, a central limit order book for the European Union Primary Dealer Network, following the appointment of MTS as a recognised interdealer platform by the European Union for the implementation of electronic market making on debt instruments issued by the European Union.”

The retail part of the fixed income trading registered a robust performance driven by sustained favorable market conditions including high inflation, rising interest rates and increased volatility.

Fixed income trading is the second largest trading segment. In this segment volumes increased in 2023 by 16% towards € 107.4M and this uptrend continues in 2024 with an 11% increase in the first quarter 2024.

As you can see there are a lot of macro dynamics which are impacting the volumes of Euronext. On one hand the low volatility in equites is resulting in a drop in volume, on the other hand the increasing rates and inflation results in more revenue for fixed income trading. As Euronext became more diversified it can partly offset a drop in one segment (cash trading) with an increase in the other segment.

Post-trade

Post-trade consists of Clearing and Custody & Settlement.

Clearing is the procedure by which financial trade settle. It is the correct and timely transfer of funds to the seller and securities to the buyer.

For Clearing Euronext just reached a new milestone: the expansion of Euronext Clearing to Euronext Brussels cash market (November 6, 2023) followed by Euronext Amsterdam, Dublin, Lisbon and Paris cash markets (November 27, 2023). This clearing was performed by LCH SA in the past and since Euronext has it’s own clearing house after the acquisition of Borsa Italia it can use this clearing house for other exchanges as well. This will result in an increase of Clearing in 2024. By digging into the Euronext figures I expect this will increase revenue for clearing by at least 20% in 2024.

Euronext Securities is the Custody & Settlement network connecting European economies to global capital markets. As part of the "Growth for Impact 2024" strategy, Euronext plans to “scale up and pan-Europeanise Euronext Securities”. In the first quarter of 2024 we have seen a further increase of roughly 4%.

Advanced Data Services

Euronext's Advanced Data Services segment generates revenue by selling real-time, historical, and reference market data to various clients. These clients include global data vendors, financial institutions and individual investors. Here's an overview of how this segment operates and its key aspects:

Real-time Market Data: Euronext sells real-time market data feeds containing trade prices, quotes, and other information from its cash and derivatives markets to data vendors and financial institutions. This is a major revenue stream.

Historical Data: Euronext provides daily historical data, end-of-day data, and corporate action data to clients on a subscription basis.

Reference Data: Euronext offers reference data products like security master files, corporate action data, and index data to clients.

Indices: As a leading provider of benchmark indices like CAC 40 (France), BEL 20 (Belgium), and AEX (Netherlands), Euronext generates revenue by licensing these indices to product issuers for creating index-linked investment products.

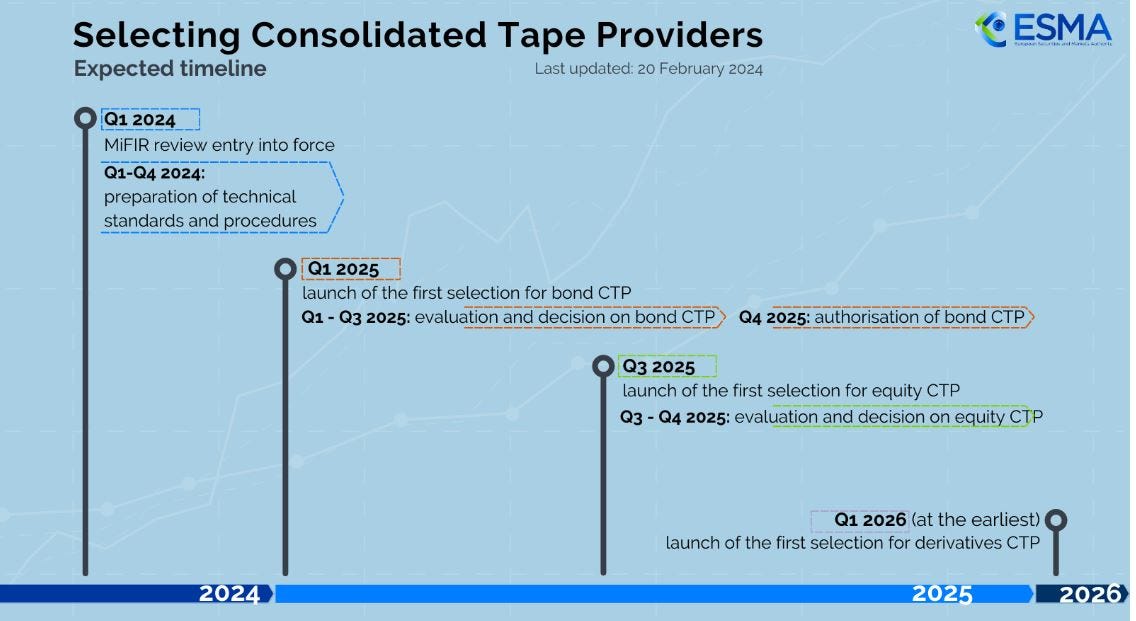

The EU has proposed a European Consolidated Tape (ECT), which could impact the revenue of Euronext. It’s important to investigate the potential impact. The ECT aims to create a centralized feed which will consolidate market data from various European trading venues. It could impact Euronext’s Advanced Data Services:

Increased competition: The ECT may provide an alternative source of consolidated European market data, potentially reducing Euronext's market share in this segment.

Pricing pressure: The ECT could exert downward pressure on market data pricing, affecting Euronext's revenue from data sales.

However, Euronext could also leverage its expertise and participate in the ECT as a data contributor or provider. In this way they will mitigate the competitive threat and will create new revenue streams. Together with other stock exchanges Euronext has created EuroCTP : a European initiative to establish a consolidated tape (CT) in the EU. But there is competition. Here is the overview when the European Securities and Markets Authority (ESMA) will launch the selection for bond CTP and equity CTP:

Source: ESMA Consolidated Tape Providers

Overall, while the ECT poses challenges, Euronext's diversified data offerings (including proprietary analytics and index products) could help offset potential revenue impacts in this strategically important segment.

Listing & Corporate Services

Companies having equity securities listed or admitted to trading on most Euronext markets are subject to the following type of fees:

Initial admission fee charges based on the market capitalization at first admission

Subsequent admission fees charged based on the amount of capital raised and calculated

Annual fees based on the number of outstanding securities

The markets for Oslo, Dublin and Milan have adopted slightly different fees.

Euronext Corporate Services offers innovative solutions and tailor-made advisory services articulated around five pillars: Governance (iBabs), Compliance (ComplyLog), Communication (Company Webcast), Investor Relations (Advisory and IR Solutions), and Corporate training (Academy). A major part of these Corporate Services products are software as a services (SaaS) solutions generating recurring revenues through annual subscriptions. In addition, Euronext Corporate Services also generate revenues on renewable advisory mandates or on one-off missions and events.

Euronext is servicing it’s corporate services over 4,800 clients in 30 countries. Without adding new stock exchanges to the group (M&A) this segment of Euronext seems to be quite stable. Last year revenue increased by 1%.

CEO / Management

Management of a company for me should be very reliable. Reliability however can be very subjective. My focus is always on the CEO, as that’s the person who is end responsible. What I am looking for is:

Business experience: Stéphane Boujnah is CEO of Euronext since 2015 and his prior working experience all have been in the financial sector, with roles in Deutsche Bank and Credit Suisse. He also has a broad network in politics, as he worked together with French minister for Economy Strauss-Kahn and was a member of the Commission pour la Liberation de la Croissance Française established by Nicolas Sarkozy.

A proven track record: Since Boujnah started in 2015 the revenue of Euronext almost tripled and increased from 0.5B to 1.4B by the end of 2023. Also earnings per share increased from 1.7 euro by the end of 2014 to 4.8 euros by the end of 2023. This is an earnings per share CAGR of 12,2% on net earnings for this period. Adjusted for gains / losses on sales of investments and assets and merger & related restructuring charges this would even have been slightly higher.

Strategy: In the Growth for Impact 2024 Strategic plan Euronext end of 2021 laid down the ambition to build the leading European market structure. They want to continue to execute disciplined and value-accretive M&A and their investment criteria is ROCE > WACC in years 3 to 5. And the good thing is Euronext really sticks to these criteria. After due diligence for potential target Allfunds, Euronext terminated the negotiations early 2023 as the criteria couldn’t be met. There are a lot of companies / managers that want to scale up their business against any price and sometimes emotion overwins ration. Euronext seems to remain objective.

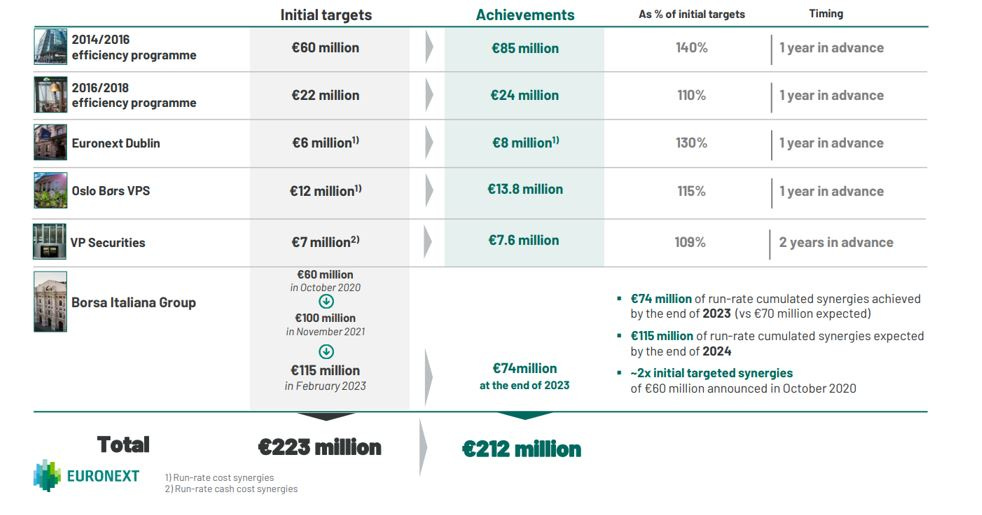

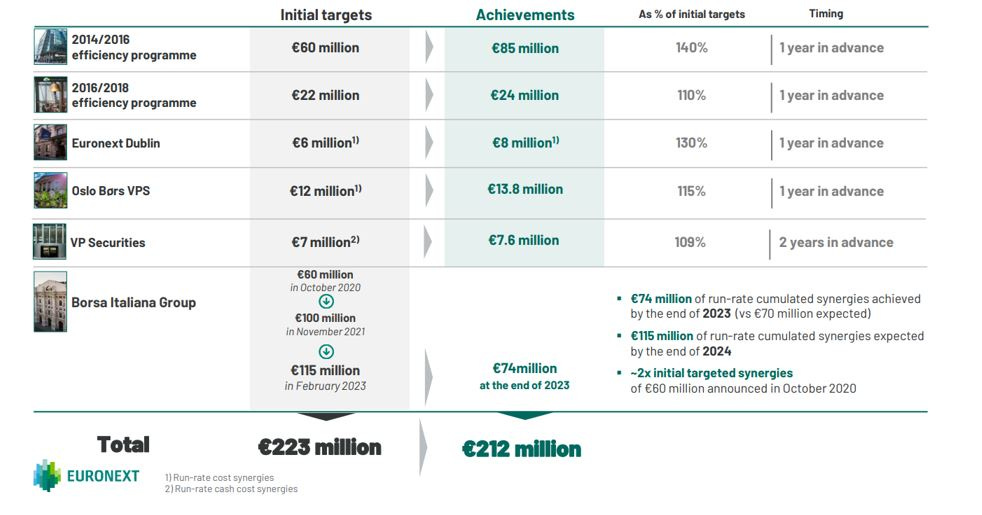

No surprises: Euronext has done a lot of M&A deals in order to build the leading European market share. An M&A deal can be a huge risk for a company, if integration fails. Euronext has proven that they are able to integrate new companies in their Group and has a unique track record of integration and operational leverage. Borsa Italia initials target in 2020 was set at €60M and they have achieved €74M by the end of 2023. Target for the total synergies by the end of 2024 is even €115M, which is almost two times the initial targeted synergies.

Source: Euronext Annual Report 2023

We now understand most of the business, although it’s quite complex if you ask me, and also know management is very reliable and capable. It’s time to have a look at financials.

Balance sheet, P&L and cashflow

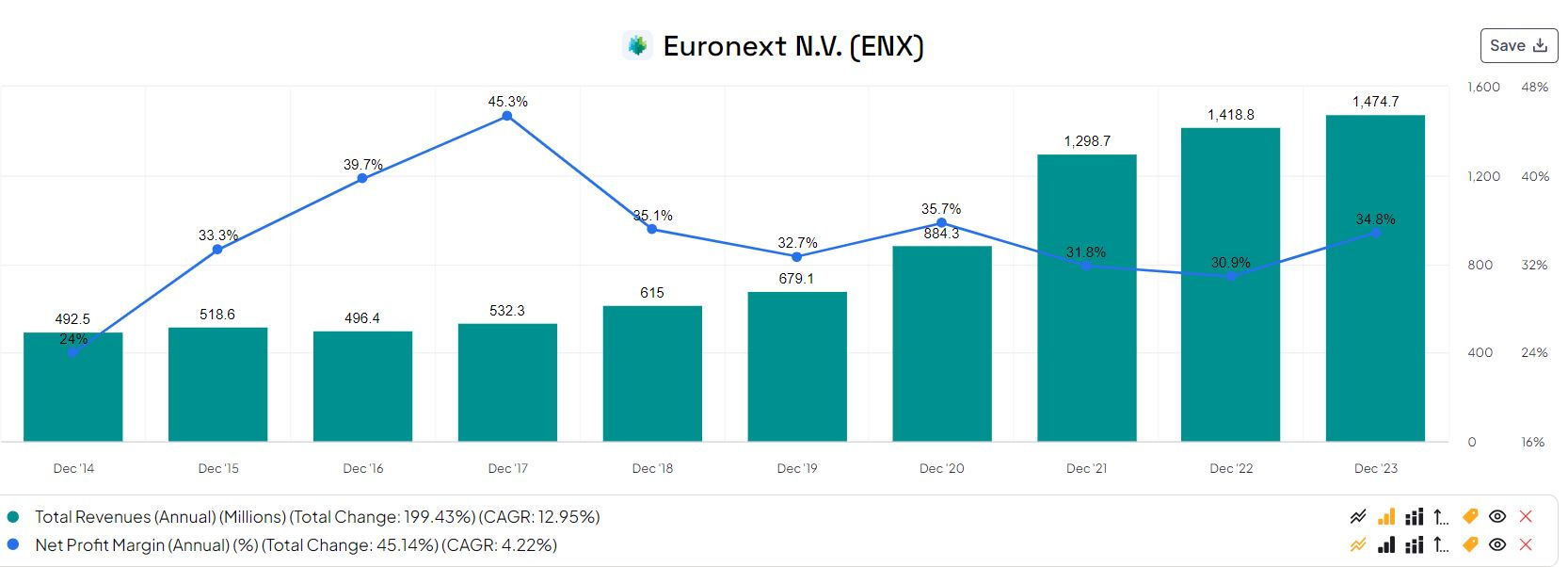

Let’s start with the P&L. Except for 2016 the revenue has been growing every year with a big increase in 2021 as a result of the acquisition of Borsa Italia:

Source: Finchat

The Compounded Average Growth Rate (CAGR) over these years is 12.95% As you can see Euronext is very profitable with a Net income margin of more than 30% (!) since 2015.

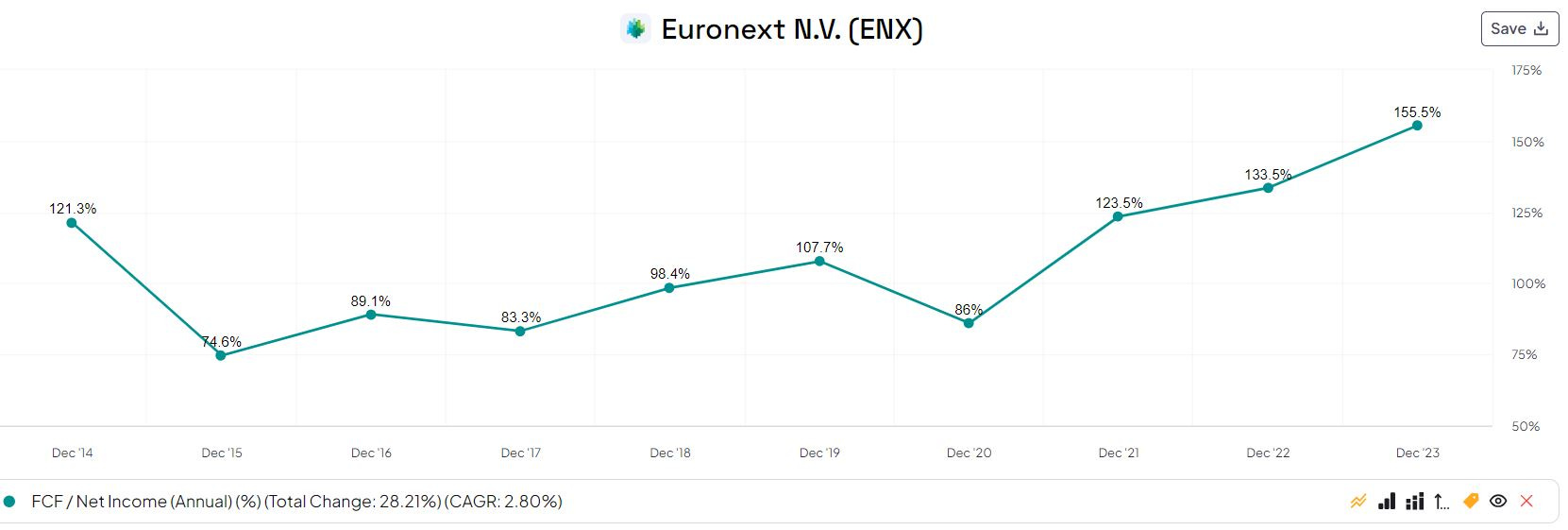

If we look at the free cash flow versus the net income, this is very healthy with the last 3 years above 100%.

Source: Finchat

Euronext pays 50% (which is just below the 3% dividend yield) dividend and since 2021 had to repay debt which was used to finance the acquisition of Borsa Italia. Their net debt at the end of 2023 stood at 1.556M euro and net debt / ebitda decreased from 3.1 in 2021 just below the 2.0 at the end of 2023.

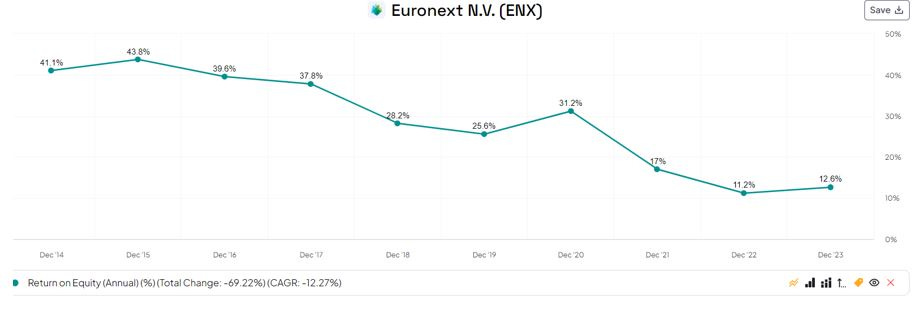

The Return on Equity for Euronext dropped a lot since the acquisition of Borsa Italia, which was paid by a combination of debt and equity. As a result the Equity increased by around 2.7B in 2021, having a significant impact on the Return on Equity.

Source: Finchat

I couldn’t find the net income figure for Borsa Italia separately, but it’s clear looking at the Return on Equity that Euronext paid a lot to acquire Borsa Italia. However, the acquisition strengthened Euronext post-trade activities by adding a clearing house, which is very valuable for Euronext. There are still integration efforts ongoing which should support to increase Net income further.

In 2023 Euronext paid 89.9M merger & related restructuring costs and had a one-off for a gain on sale of investment of 57.5M. If I would exclude these I come to an adjusted Earnings per share (EPS) of EUR 5.27. Euronext is reporting an adjusted EPS over 2023 of EUR 5.51. The difference is probably the provision Euronext made of €36M for the termination of the LCH SA clearing agreement.

In 2018 the adjusted EPS was EUR 3.44 per share and with EUR 5.51 in 2023 the CAGR last 5 years is at 9.9% This is lower than the growth in revenue (5 year CAGR of 19.11%) and I expect this is the result of a lower margin for Borsa Italia versus Euronext stand-alone (excluding Borsa Italia). Euronext is strong in cost control and synergies and as they are still going through the integration of Borsa Italia I would expect we should see this reflected in EPS coming years.

Now Euronext is back to Net debt / ebitda level of below 2, they have room for acquisitions or share buybacks. In recent earning calls they were pointing a bit towards share buyback, but more will become clear with their strategy update in November 2024.

As mentioned before, Euronext paid a lot for Borsa Italia, as a result the goodwill position on their balance sheet (close to EUR 4B) almost equals the total Equity. If I would deduct the goodwill from the equity, we still have a positive equity. In general I prefer to see a lower goodwill balance, on the other hand Euronext has bought another monopoly exchange with their acquisition in Italy. The goodwill paid for Borsa Italia is close to 3B.

Valuation

As always I will run a Discounted Cash Flow Model to determine the current value. In my model I am using a yearly 4% growth of the revenue (this year 5% because of the higher clearing revenue), an operating margin of 52% and a WACC of 8.5%. With a terminal growth rate of 2.5% I get to an equity value of 10.4B or 101.5 euro per share, which is around 19.7% upside. For a quality business like Euronext a discount just under 20% is interesting. In my opinion the risk is very low (rule number 1: don’t lose) because of the wide moat and the recession proof business, while there are potential triggers which could increase the valuation like:

Further synergies and revenue increase because of the integration of Borsa Italia

Bolt-on acquisitions or share buybacks, which I didn’t include in my valuation

Potential market volatility, which is good for Euronext volume related revenues

Launch of Euronext Mid-Point Match offering dark, mid-point and sweep functionalities as of April 2024 not included in the forecast. Requested Euronext for an indication of revenue, but they don’t want to share it yet.

Current forward P/E for Euronext is around 14.5 (P/E 17.91 for last 12 months), while London Stock Exchange Group (LSE) has a forward P/E of around 25.5 and Deutsche Boerse a forward P/E of 17.1. If LSE or Deutsche Boerse had higher margins, I could understand the difference, but compared to both Euronext has higher net margins and a higher Free cash flow margin. Out of these three companies, Euronext in my opinion is the best investment. I like the margin of safety, so my Buy-Below price is 85 euro.

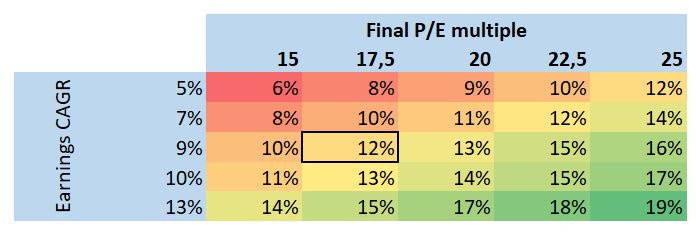

Here is the heatmap, with the expected return per year of 12%, where I calculate with a P/E of 17.5, although the DCF-method shows me the realistic P/E is 20.

Risks

Credit risk: Euronext manages substantial credit risks as part of its operations, including unmatched risk positions that might arise from the default of a party to a trade

Credit risk: As a central counterparty clearing house (Euronext Clearing), Euronext faces counterparty credit risk from clearing members

Operational risk: Euronext's operations rely on the secure processing, transfer and storage of confidential and other information in computer systems and networks. Any cyber security breaches, data corruption or operational errors could have adverse impacts

Legal & Compliance risk: Changes in laws, regulations or government policies could materially impact Euronext's business, financial condition and operating results

Strategic and business risk: Execution risks around Euronext's strategic objectives, including the integration of acquisitions like Borsa Italia

Financial risk: Exposure to market risk factors like interest rates, currency rates, credit spreads that could impact financial results

The annual report highlights Euronext's comprehensive enterprise risk management framework to identify, assess, manage and monitor these key risk categories across the company's operations and activities. Robust risk controls and mitigation measures are implemented.

Summary

Very strong moat business and recession proof

Reliable and experienced management

Strong in M&A, integration and realizing synergies

Non-volume share increasing with recurring revenues

Expansion of Euronext clearing

Launch of dark, mid-point and sweep functionalities as per April 2024

Net debt / Ebitda ratio below 2: M&A potential and share buybacks (not considered in the case)

Very healthy net margins

High goodwill balance because of Borsa Italia acquisition

Current undervaluation of close to 20%

Typical “don’t lose” stock for the long-run and a backbone in my portfolio

Did you like this analysis? Share it with your friends!

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.

Well Written Arnold: I owned the company but sold it since the takeovers are not always adding value for shareholder. Prefer NASDAQ and OTCM