Nedap: Technology For Life. Extremely undervalued. Buy Now Hurray Later.

Nedap: Technology For Life. Extremely undervalued. Buy Now Hurray Later.

Nedap is a Dutch high-tech company with a very bright future ahead. I have add Nedap to my portfolio and made it my biggest single position.

Introduction to Nedap

Nedap has seen a transformation since their CEO Ruben Wegman came at the helm in 2009. Till 2009 Nedap didn’t have a real focus and their philosophy was “many flowers grow”. However Nedap already made the change to focus on software in 2000 and they started applying innovative RFID technology in practice since 2003. This laid the foundation for Nedap today, with four core technologies: connected devices, communication technology, software architecture and user experience. Their business units Healthcare, Security, Retail and Livestock seem completely different, but they all have in common that the technology behind is similar. The revenue is generated from sales of products and systems (non-recurring), from software subscriptions (licenses) and from services sold (recurring). There is focus to increase recurring revenue as part of total revenue over the years. It all starts for Nedap with a deep knowledge of their markets and they idolize technology. Building their own solutions and market them also means that Wegman prefers to grow autonomously. M&A is seen as risky, because of the cultural difference and potential differences in technology. But there can be exceptions for M&A. Before Wegman became CEO of Nedap in 20009 he was already seven years part of the Board.

A couple important changes Wegman introduced:

Focus on the added value per employee.

Introduction of “Power to the People” with the outcome that employees can become shareholder of their own company (skin in the game).

No development for clients anymore, but own in-house development.

Having own products means having pricing power.

Setup of an AI task force (since March 2023) which aims to facilitate the adoption of AI throughout Nedap.

Instead of building solutions for customers (paid by the hour), Nedap is now focusing on building their own solutions. With their deep market knowledge in the different business units and their technology knowledge (RFID), they have proven to create products / software which is better than their competitors. Good to know is that Nedap is not activating software costs on their balance sheet. A lot of companies tend to do this, but Nedap takes these development costs directly into their P&L. This means no risk on write offs of software.

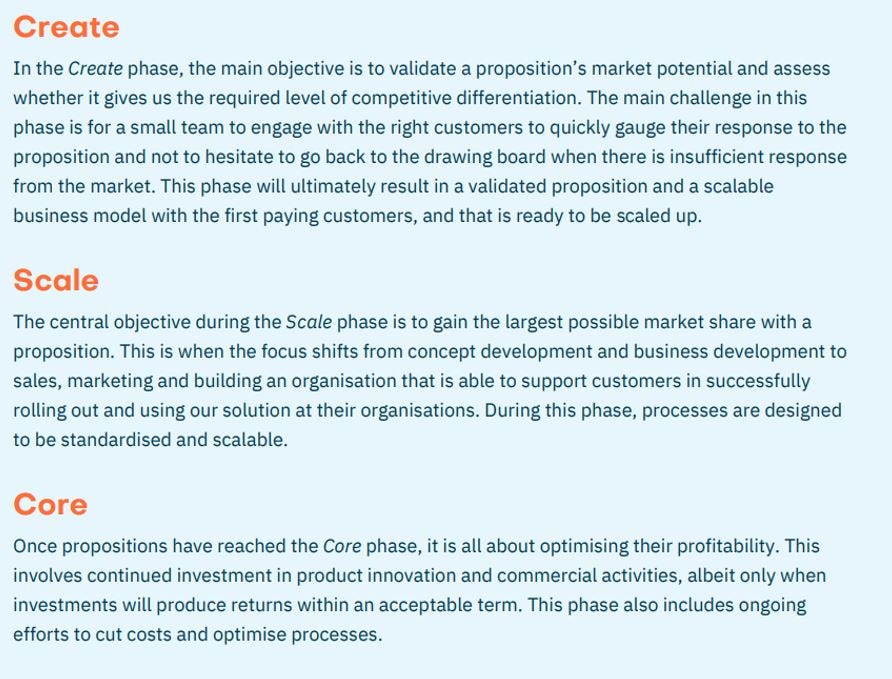

Since 2019 the strategy is called Step Up, with a focus on reaching market leadership in the businesses Nedap is active. They use a Create-Scale-Core model:

Source: Nedap Annual Report 2023

This model is important, because Nedap wants to have the ability to scale-up rapidly, which results in a greater focus on a limited number of propositions. As a result sometimes Nedap chooses not to go for a market opportunity. An example is a solution to prevent shoplifting. Although Nedap sees an opportunity, they see a booming opportunity in Retail for RFID, where they support perfect inventory visibility for customers. Their full focus in Retail is in inventory management and they want to be the market leader in this area. Especially in the United States they see huge opportunities and they have build a dedicated local team. I like the focus of Nedap and also that they don’t go for each opportunity, in this case the shoplifting prevention opportunity. As a shareholder it feels they really do the right things.

The financial targets from the Step-Up Strategy towards 2025 are:

Autonomous revenue growth of 8 to 9% annually

Operating margin, excluding one-offs, of 15%

ROIC that outgrows profitability

Net debt / Ebitda of 1.5 maximum

Solvency rate of at least 50%

Profits paid out to shareholders after deduction of amount needed for investments in profitable growth and the intended financial structure

Source: Nedap Annual Report 2023

What I like to see is companies which focus on ROIC and on autonomous growth. Both are the case. The operating margin target of 15% will be achieved probably in 2026. Nedap has invested a lot in employees and scalability last years, which has been a strategic choice for the long-term. What I like from Wegman is that his focus is not short-term, not even four years, but he looks for the best path long-term.

Lets have a look at the main four business units.

Healthcare

Nedap wants to improve healthcare by supporting healthcare institutions in the Netherlands in planning, registering and administering care. They want to make a sustainable difference for all the employees in healthcare. They have 4 solutions:

ONS Software is an integral software package which should simplify all administrative tasks for healthcare professionals. More than 1.500 healthcare institutions and more than 300.000 healthcare professionals already use ONS. ONS is used with elderly care (nursing homes, care homes and home care organizations), disability care and mental healthcare.

Luna software helps to easily structure the daily lives of people with cognitive problems. People using Luna often get the costs reimbursed from the health insurer.

Caren. ONS software customers automatically also receive Caren. Caren is a digital health file and a communication platform on top. More than 400.000 people use Caren on a daily basis to organize care for themselves or others.

MediKIT – general practitioners (GP) information system. Here Nedap made an exception and recently acquired MediKIT. MediKIT has been developed by a GP who thought software really could be different and better for GPs. Nedap learned about this start-up and recognized the software as truly amazing. Also within the GP market the potential is huge. Together with Nedap MediKIT will penetrate the market.

With these solutions Nedap is the market leader in the Dutch healthcare market, where more than 1,700 healthcare organizations as a customer. Nedap will scale their solutions further and sees excellent opportunities for MediKIT to start scaling in the general practitioner market. First GPs have already chosen for Nedap and more to come. The new software will play an important role for Nedap to play a leading role in network care. MediKIT is operationally since last year and the GP market is one where Nedap has new growth opportunities in a key market.

I have analyzed the mental healthcare in The Netherlands in more depth. Together with competitor Avinty, Nedap is in a fight for market leader. In 2023 Avinty was the number 1 in the market. Nedap was unlucky that in size some of their customers fell out of the top 50 mental healthcare organizations, while Avinty customers grew in 2023. The last 2-3 years Nedap has won 6 tenders (GGZ Drenthe, GGZ Eindhoven, Arkin (co-supplier), Lentis, Reinier van Arkel and Trajectum), while Adapcare won two tenders and Nexus and Tenzinger both won one. Six out of ten, which is a win-rate of 60% within the top 50 mental healthcare organizations. Nedap is gaining market share rapidly. In the four cases Nedap didn’t win, they weren’t the current software supplier. Retention rate is high. Nedap announced this year they have won GGZ Eindhoven. Nedap is close to a market share of 27%, while Avinty just beat them in 2023. It’s very likely that Nedap will become market leader in 2024, given the win of GGZ Eindhoven.

Retail

The Nedap iD Cloud Platform supports to always have product availability at the right place and time. The platform creates a complete and transparent view of the supply chain for the customer. Nedap used it Software as a Service (SaaS) experience from Healthcare to become a global leader in the market for RFID-based inventory management systems. Customers pay a monthly fixed amount per location / shop, which results in recurring revenue. Nedap has been rapidly growing in this market with (global) customers like Lululemon, Boss, PVH, Puma, FootLocker, Puma, UnderArmour, On, Adidas, River Island and Woolworths. Pacsun was add in January 2024.

The Compound Annual Growth rate for the RFID Inventory Retail Management Market is projected at 8.5% to reach $1350M by 2032. Top key players are: Nedap Retail, RIOT Insight, Uniqueid, Retail Reload and Hopeland Technologies.

Source: Pulse RFID Inventory Retail Management Market

Nedap has a leading role in the market of RFID solutions for retailers, which it expended further in 2023 towards around 60% market share. The retail market in the second half of 2023 and first months of 2024 has been difficult, but Nedap expects revenue to increase with excellent growth opportunities in the coming years as Nedap is an early adopter and the market is still in an early phase.

Security

The security business unit focuses on access control and security systems for companies and institutions worldwide. It has 5,838 enterprise clients and opens almost 50 million doors each day. More than 25% of all major brands headquartering in Europe use Nedap’s AEOS access control system.

In Europe and the Middle East Nedap is the leading provider of solutions managing physical access to premises. Nedap continuously invests in product innovation, which has led to the launch of two new propositions in 2023. Access AtWork offers a SaaS-solution which responds to the need for scalable and secure access control in the form of a service. The proposition has been implement at the first organizations. The second proposition is Pace, which supports organizations to maintain an overview of all access rights and ensure everyone has the correct user access rights. Pace works as an overarching system for all access control systems at multiple sites and stands for Physical Access Control for Education. It’s a clear focus to secure property in the education sector.

For 2024 Nedap expects similar revenues as in 2023, mainly due to the catching up of delivery backlogs in the first half of 2023. “The global building access control security market is expected to display a CAGR of 14% in the period 2023-2033. The increasing demand for smart building and infrastructure will be driving the demand for the building access control security market in the future.”

Source: Global Building Access Control Security Market

Livestock Management

Livestock is about dairy farming and Nedap believes individual cow care improves the performance and wellbeing of the entire herd. The technology of Nedap is used by thousands of farmers to monitor millions of cows every day. The business units has three solutions:

CowControl: all-in one monitoring

FarmControl: manage the entire herd

MilkingControl: milk quality and milking speed

Nedap has scaled down their pig sector activities and will fully focus on the growth opportunities in the dairy sector. Nedap Now is the cloud based platform for all three solutions used by farmers. It shows a health score giving insight in the health of cows, a heat score for the heat of every cow and heat stress, which has just been added recently. For heat stress farmers pay an additional fee. It shows heat stress experienced by the cow. Using Nedap Now, dairy farmers and Nedap continuously are in direct contact. Internally the Nedap has a target for Nedap Now to add a new functionality every six weeks. In this way they keep on improving the platform and stay ahead of competition.

About the market for Livestock Nedap says: “Market data supports our estimate that in the coming years, the adoption of technology for automated identification and monitoring of individual animals on increasingly larger farms will accelerate. It is therefore crucial to ensure that the organisation is ready to capitalise on this growth. In 2023, we continued to intensify our investments in our commercial and support organisation globally. This resulted in us having our own employees on all continents who can support our partners with professional marketing and support materials.”

Source: Nedap Annual Report 2023

Wegman clearly mentioned they see opportunities in New Zealand and there has been a lot of effort to build a team over there, so they can grow the business.

In 2023 Nedap started offering SmartTag as a Service, where the farmer is billed monthly through Nedap Now. Farmers can switch to advanced Nedap technology , where the monthly costs of the Nedap solution can be funded from the higher yield per cow that results from Nedap technology. This is another example which supports the target of an increase in recurring revenue.

For the full year Nedap expects revenue growth for the business unit LiveStock Management, with the largest revenue contribution in the second half of 2024. “The global dairy herd management market size was valued at USD 3.11 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 7.1% from 2023 to 2030.”

Source: Dairy Herd Management Market Size

Overall view

Nedap is clearly building and enhancing platforms in multiple business units with the ONS platform in Healthcare, the iD Cloud platform in Retail, the Now platform in Livestock. I understand their business and they will see tailwind coming years because of secular growth: care, security and digitalization. Licenses and subscriptions to their solutions will give them more and more recurring revenue. Being or becoming market leader gives them pricing power on top. With the create – scale – core model Nedap clearly defines in which phase they are. Most of the businesses are in the scale phase, which means they are investing in growing and scaling their business and not yet in optimizing the profitability. I think it’s good to be an early investor in Nedap. At the time they will reach Core phase for their solutions, the recurring revenue is high and margins will increase, which means valuation of Nedap will increase too.

Balance sheet, P&L and cash flow

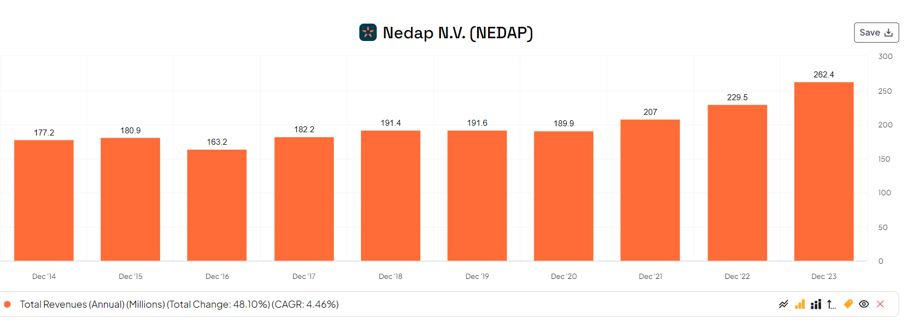

I think it is good to start with an overview of the revenue last years.

Source: Finchat

Revenue as per December 2023 stood at 262.4M and the CAGR has been 4.46% over the years shown. This is not a compelling CAGR, but Nedap has seen a huge transformation. They sold or exit Nsecure, Nedap France and Nedap Beveilingstechniek (Security Technics), Pigs (in Livestock) and currently Flux business unit is also identified as “not a fit”. All these activities had revenues and stop doing these had and will have impact. But they are almost there with transforming their business and revenues are expected to grow by 8 to 9 percent on a yearly basis. Given the expected market growth CAGR I could find, I think this is a very realistic target. If we just look at the last three years, the CAGR has been 11,4%.

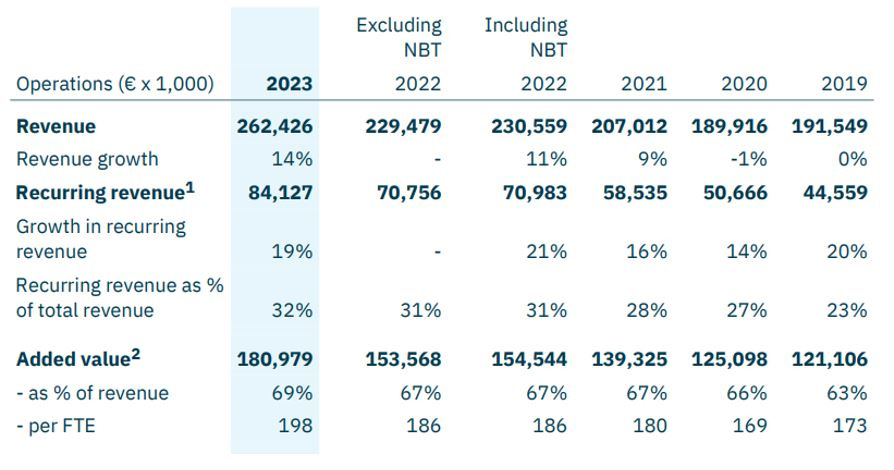

Nedap wants to grow in recurring revenue and in 2023 this was 32% of the total revenue, compared to 23% in 2019. I expect this can grow towards 40% in 2030. In the below overview you can also see the added value per FTE has grown from 173k in 2019 towards 198k in 2023.

Source: Nedap Annual Report 2023

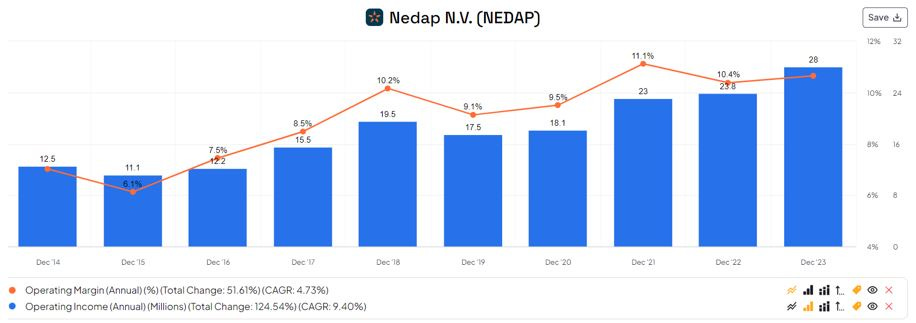

The target for operating margin of 15% is expected to be reached in 2026.

Source: Finchat

Current operating margin is 10.7%. As mentioned earlier, the focus on scaling the business result in a lower margin as they had to grew their teams to be prepared for new customers and be able to service them in a proper way. Below the SG&A to revenue percentage, where it is clear this jumped to an elevated 42.7%.

Source: Finchat

Management has communicated clearly this had to do with scaling the business and growing the teams and we can expect this percentage to decrease to more normal levels coming years. Barring unforeseen circumstances, I have no doubt they will increase their operating margin towards 15% in 2026 and longer run, given the nature of the business, I expected they will further increase their operating margin.

What I also like to see is although figures are impacted by the divestments of parts of the business and hance revenue CAGR has only been 4.46%, the operating margin CAGR outgrow the revenue with a CAGR of 9.40%.

The Return on invested capital is an important metric as it determines how well a company allocates its capital. In my calculations ROIC in 2023 stood at 27.4% and will increase further coming years as a result of the increase in operating margin.

The only downside I currently see with Nedap is that they don’t see opportunities to invest most of their cash in the business. Almost all the cash is paid out as dividend. Wegman says that they hardly see opportunities and think they can better grow autonomously instead of M&A. If he asks managers to invest 100k, they don’t see options to spend it wisely. Nedap is a capital light business, which I like. The only thing is I have to reallocate the dividend myself, but I will find a nice place!

Nedap has a little bit of debt on their balance sheet, with a current net debt / ebitda of only 0.15. Current assets are more than twice current liabilities. As mentioned earlier they don’t capitalize software development and they don’t carry any goodwill on the balance sheet. Conclusion: the balance sheet is very healthy.

Valuation

Management gave a guidance on revenue growth of eight to nine percent annually. As 2023 has a tough comparison due to the delayed deliveries from 2022, I will calculate with 8.0% for 2024 and with 9.0% for the years after. I expect this is conservative as I expect Nedap to grow faster than the market.

The long-term growth rate I have put at 2.5% and I have calculated a weighted average cost of capital (WACC) of 7.73%. I will use the expectation that operating margin will grow towards 15% in 2026. This gives a valuation of 118,75 per share for 2024, which is a 90% undervaluation compared to the current stock price of 62.60 euro. This clearly indicates the undervaluation of small caps in Europe and the market not understanding the transformation process of Nedap. A company with high recurring revenue, which is market leader in multiple markets and which the product differentiation of Nedap, should deserve a much higher valuation.

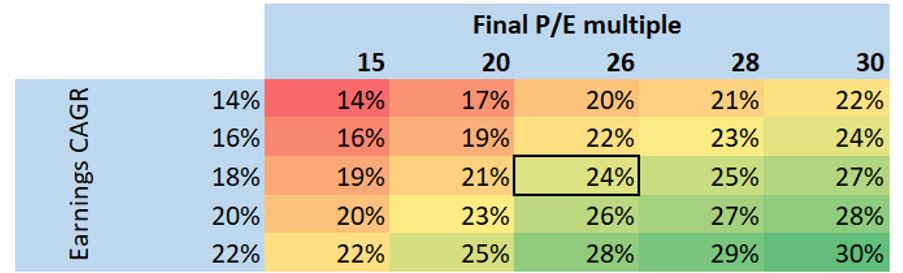

When I assume the dividend will grow, but the dividend yield will drop because of the higher share price, I get to 2.2% dividend annually. Assuming a P/E of 26 after ten years and adding the 2.2% dividend the annual expected return is 24.4%. I will share the heat map to see what happens if earnings CAGR comes in lower, e.g. at 14% and P/E would drop to 15 (worst case scenario). I still would get an annual return of 14%. The margin of safety is very high.

Risks

Finally it is good to shortly go over the risks associated with an investment in Nedap:

AI will create market opportunities but at the same time goes accompanied by new risks. That is why Nedap introduced the AI taskforce (High)

Unsuccesful proposition and product development (High)

Potential shortage of talented employees (Low)

A successful cyberattack resulting in damage to Nedap (Low)

Geopolitical conflicts: Nedap relies heavily on Taiwan for semi-conductors (Medium)

Delay or aborted delivery of products and supply chain dependence (Medium)

Inability to achieve sustainability goals (Low)

Insufficient access to or insufficient implementation capacity at customers (Medium)

Compliance risks like fines, sanctions or damage to reputation (Low)

All of the above mentioned risks are part of the risk framework of Nedap. For each single item they are monitoring and mitigating the risk. E.g. the AI risk is tried to be mitigated by Nedap through the implementation of an AI taskforce. Towards the potential of shortage of talented employees I like to mention that I like the culture of Nedap, with limited management layers, employees don’t have to account for hours, no performance reviews and assessment reviews and unlimited days off, as long as it’s arranged within the team. This results in a lot of own responsibility.

Summary

In my opinion the case for Nedap is rock solid. I have made it my biggest position in my portfolio. Summarized:

Four business units, all targeted to become market leader in their area

Management with a long-term focus

Autonomous growth

Employees with skin in the game and high own responsibility

Operating margin expected to grow above 15% in 2026

Recurring revenue growing, making the business case more predictable

Secular growth in care, security and digitalization

Very healthy balance sheet

Extreme low valuation with 90% upside

Buy now, hurray later!

If you like this article, please give it a thumbs up or share it on social media!

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.

Sounds good and I might dive in deeper here too. However the valuation seems pretty optimistic. I'd never use a discount rate below 10% personally (I'm not a fan of the "scientific" way to calculate a WACC). 14% earnings CAGR as a worst case is also optimstic imo.

Quality analysis. Been a shareholder for some time now and can't wait for them to capture more growth in while raising the margins.