LibertySiriusXM: A Value Play With A 35% Discount

LibertySiriusXM: A Value Play With A 35% Discount

When I read Berkshire was heavily buying into this business, I had to understand why.

As a quality investor I invest in companies with strong management, strong market positions (MOAT), businesses which are growing and with strong quantitative criteria like ROIC and free cash flow. But sometimes you come across a value play which you just can’t ignore. LibertySiriusXM is such a play.

Liberty SiriusXM – the company

The Liberty SiriusXM Group is a holding company with an ownership of approximately 83% in SiriusXM. It’s good to understand the business of SiriusXM first. “SiriusXM is the leading audio entertainment company in North America with a portfolio of audio businesses including:

its flagship subscription entertainment service SiriusXM: 34 million paid subscribers.

the ad-supported and premium music streaming services of Pandora: over 50 million active users and 90 million monthly digital audio listeners.

an expansive podcast network: 45 million monthly listeners; most shows ranked in top50 and number 1 podcast network with women.

a suite of business and advertising solutions.

Source: website SiriusXM

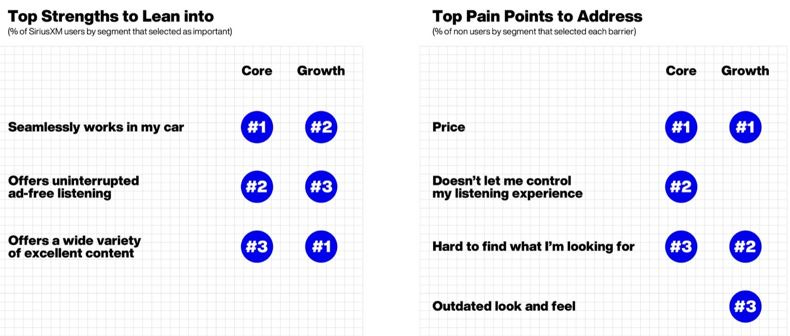

Reaching a combined monthly audience of approximately 150 million listeners, SiriusXM offers a broad range of content for listeners everywhere they tune in with a diverse mix of live, on-demand, and curated programming across music, talk, news, and sports.” They have a strong core of loyal and passionate subscribers. However, their customers see strengths, but also some pain points:

Source: Lippincott Segmentation Study 2022

According to the Liberty Investor Day Presentation SiriusXM tried to address the pain points:

Newly redesigned, easy to use, modernized client applications.

Improved search and discovery.

Improved sports and talk experiences.

New commerce and identity platforms.

Martech enablement through implementation of Salesforce.

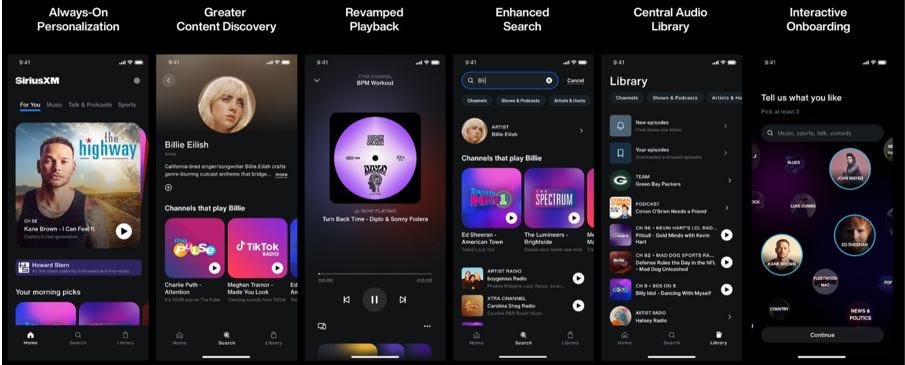

And they also shared the new look and feel:

Source: Liberty Investor Day Presentation 2023

They have made it more like a Spotify or Netflix feel. All these functions are available as of December 2023. SiriusXM 360L is their newest and most advanced audio entertainment platform. They want to tap into new audience and grow with their Next Gen Platform. The younger and more diverse audience has limited experience with SiriusXM, while their core audience is highly satisfied and shows low churn.

One of the strengths of SiriusXM is their availability in 80% of all new vehicles and 55% of the pre-owned vehicles currently sold. Of the new Sirius XM vehicles now 33% is equipped with 360L. Having their platform available in so many vehicles is fantastic. The automakers receive a share of the subscription profits, so SiriusXM created a win-win situation. The more subscribers, the better also for the automakers. SiriusXM has signed long-term contracts with automakers within US and Canada:

Toyota (all models cars, trucks and SUVs) till 2028

Ford Canada till 2025 (couldn’t find Ford USA)

General Motors (Chevrolet, Buick, GMC, Cadillac) till 2027

Stellantis (Chrysler, Jeep, Dodge, Ram, Alfa Romeo, Fiat and Maserati) till 2027

Mercedes Benz USA multi-year expension signed in 2023

Nissan North America till 2028

New car owners can opt in and activate a couple months free SiriusXM trial subscription. Having signed multiple long-term contracts with automakers raises the question whether they will keep satellite in their cars for the long run or whether they will drop it. Electric vehicle manufacturers as Tesla and Rivian decided to drop the satellite route and to choose for an audio streaming service. However, Rivian announced in December 2023 to launch SiriusXM in their R1T and R1S models in 2024, which is great news. Probably a result of the new design of the 360L.

Also SiriusXM has signed long-term Sports and News broadcasting agreements, which attracts a specific group of subscribers. A couple examples:

NHL till 2028 – 2029 season.

MLB through the 2028 season.

NFL through the 2027 Super Bowl.

Nascar multiyear broadcast extension announced in 2023.

Fox News new long-term broadcast agreement announced November 2023.

PGA Tour multiyear extension announced in 2022.

Next to Sports & News they host exclusive shows and podcasts and exclusive and homegrown music channels.

Subscribers

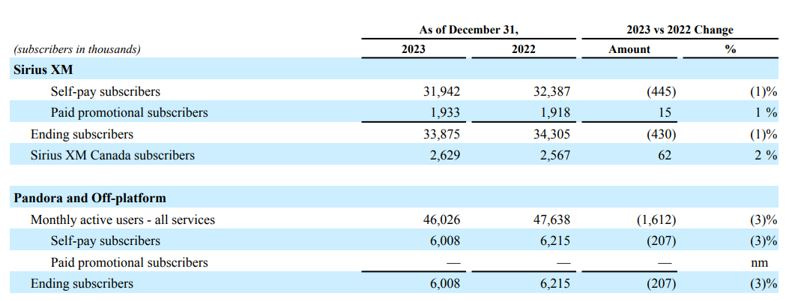

Having SiriusXM available in cars still doesn’t mean it results in subscribers. Let’s have a look at the latest trend on subscribers:

Source: SiriusXM 4Q and full year results

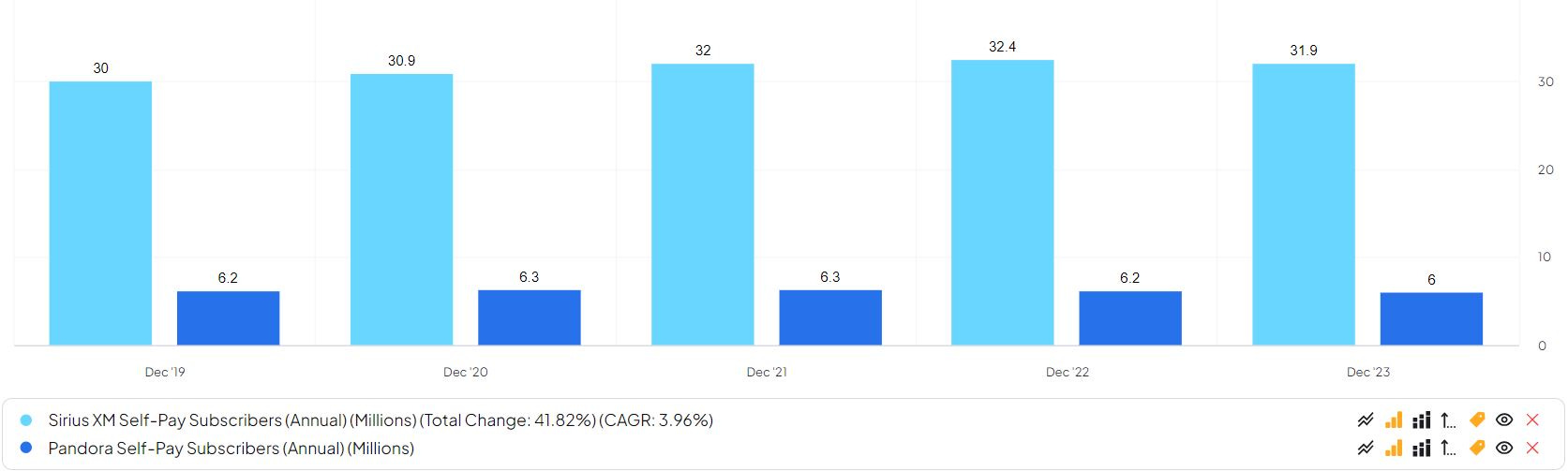

Compared to last year Sirius XM Ending Subscribers decreased by 1% and Pandora Ending Subscribers decreased by 3%. At the same time companies like Spotify and Alphabet (YouTube Music) presented high increases in number of subscribers. Within the fourth quarter 2023 SiriusXM added 131,000 new self-pay subscribers, but the paid promotional subscribers were down 225,000 in Q4. It will be interesting to see whether the new functions and look and feel of the 360L will have a positive effect and can change last-year trend in the coming quarters. The trend since 2019 for SiriusXM self-pay subscribers has been slightly up and for Pandora quite flat, with only a slight downturn in the last year:

Source: finchat.io (figures in million)

SiriusXM has a moat in satellite, however it can be substituted by streaming services, although satellite has the advantage it provides consistent coverage across large geographic areas. Also satellite radio boasts high-quality sound. The streaming services competition is fierce with cash rich tech-companies like Alphabet, Spotify, Amazon and Apple.

Structure and merger

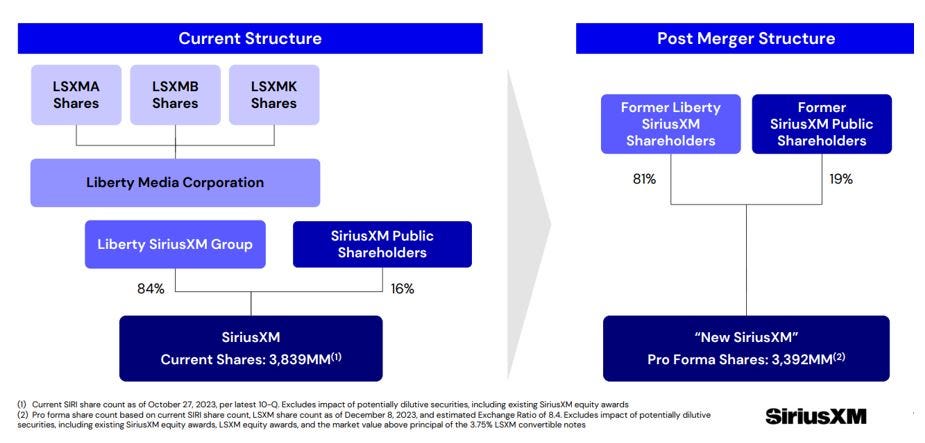

The current structure of Liberty Sirius XM is quite complex. Liberty Sirius XM consists of three types of tracking shares:

LSXMA with 1 vote per share

LSXMB with 10 votes per share

LSXMC with no votes

Going forward I will name these three trackers LSXM and SiriusXM Holding I will name SIRI.

These tracking shares are tracking SIRI and they currently own 84% of the shares in SIRI. SIRI is publicly listed and the shareholders here own 16% of the company. In December last year the companies announced a transaction to simplify their structure. In the graph below current and post-merger structure are explained:

Source: SiriusXM Management presentation 2023

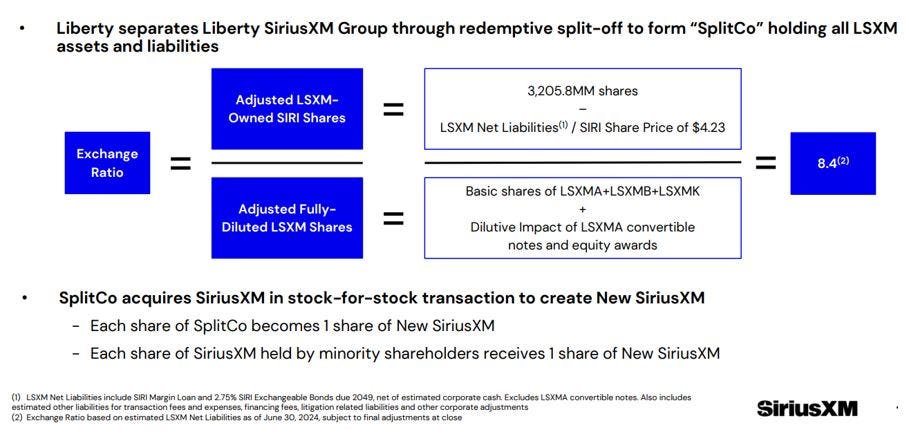

The LSXM shareholders will own 81% of the New SiriusXM and SIRI shareholders 19%. The new company will have 3,392M shares outstanding. The transaction is quite complex. First LSXM will form a SplitCo which will hold all LSXM assets and liabilities of the three tracking shares. Immediately after the split-off the new SplitCo company will acquire SIRI in an all stock transaction and together they will form New Sirius XM. Existing shareholders of the 3 tracking shares will receive 8.4 shares in New Sirius XM for every share they held, while the SIRI shareholders will receive 1 share. This exchange ratio of 8.4 is determined based on below calculation:

Source: SiriusXM Management presentation 2023

The SIRI share price of $4.23 mentioned in the calculation above is a fixed price and was determined based on the average price on 20 consecutive days before Liberty filed a 13-D Form with the SEC. The net liabilities of LSXM are estimated, so this amount could change, but I don’t expect a huge change here. On the denominator side no change expected, so the 8.4 ratio is a valid ratio to calculate going forward.

The reasons to perform this transaction is to reduce the complexity, but also to get rid of the holding discount that existed. The tracking stocks were at a discount compared to SIRI.

When the transaction was announced on December 12, the closing price on December 11 of SIRI was $5.02. Same tme the closing price of LSXMA was $26.64, of LSXMK $26.80 and LSXMB $26.56. When multiplying the $5.02 with the expected ratio of 8.4 we would get to $42.17. This means that at the time of announcement on December 12 there was a huge discount for the tracking stocks. Investors analyzing this deal at the time have recognized this arbitrage and what likely happened is that they went long LSXM shares and short SIRI. When the arbitrage disappears then one of the two (or both) sides should result in a profit. This increased the short percentage of the free float of SIRI to close to 22%. This arbitrage could have been a reason for Berkshire to add LSXM shares, although I couldn’t find they took a short position SIRI.

Now, four months later, it’s nice to see how the shares performed. What I had expected is the LSXM shares to increase to close to $42.17. But the opposite happened: the SIRI shares dropped. SIRI share at April 26th stood at $3.02, while the LSXM tracking shares were trading around $24.30. SIRI price dropped with 40% and the tracking shares dropped with around 9%. So the net result of short SIRI and long LSXM made a whopping 31% profit. The arbitrage is gone, as the stock prices are close to the 8.4 ratio. Unfortunately I wasn’t aware of this deal before, because this is serious money in just a couple of months.

But maybe it isn’t too late yet. I expect current positions (short SIRI and long LSXM) won’t be closed till the merger, unless investors rate the company undervalued, with a result that the short SIRI is bought back.

Let’s have a look whether SIRI and LSXM at current prices are strongly undervalued or not?

Valuation

Let’s start with the revenue trend. Since 2014 this trend has been upwards, except for 2023 when there was a -0,6% decline.

Source: finchat.io

Revenue trend follows the subscriber trend in the last year. Question is whether this is temporary or whether the business starts declining. I am especially curious after the changes in December 2023 with 360L how the trend will look. Given the fact that new vehicle users get a 3 or 6 months trial we might not see an impact before 3Q earnings.

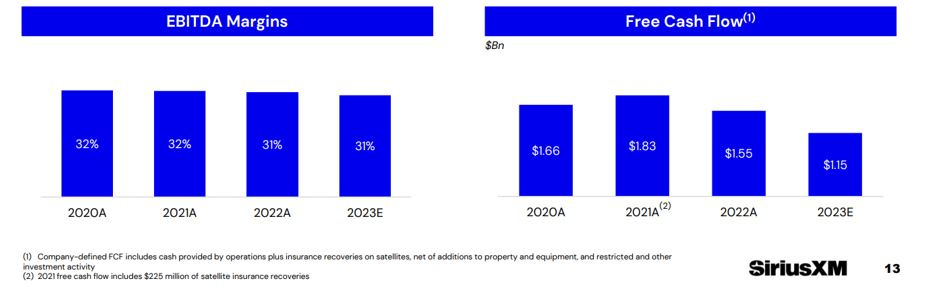

When we look at EBITDA and Free cash flow the last years SiriusXM has delivered consistently strong results and has continuously invested in their platform and listening experience. The Free cash flow generation also has been strong.

Source: Management presentation December 2023

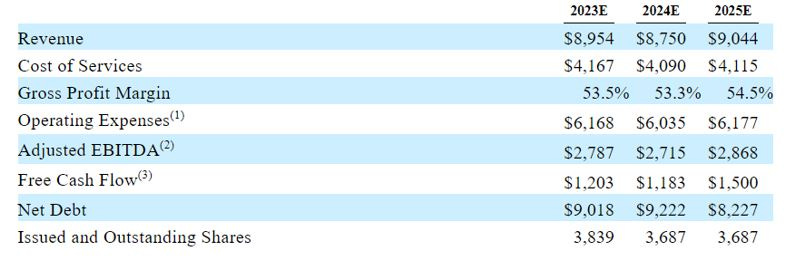

In the Form S-4 filed by the company with the SEC on January 29th, 2024 we can find the financial projections for 2023 – 2025 for Sirius XM Holding:

Source: Form S-4 filed with the SEC on January 29, 2024

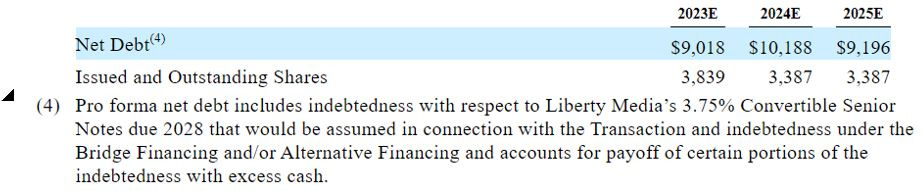

And assuming the consummation of the proposed transaction the expected debt and shares outstanding:

Source: website of the SEC

As you can see the amount of debt is quite high. This is because the dividend paid to shareholders and the share buybacks where higher than the free cash flow in last years. This means SIRI aggressively bought back shares in a low interest environment. As a result SIRI has a negative shareholders equity. Also Net debt / EBITDA stood at 3.6 at the end of 2023 and is expected to reach 3.9 at the time of the merger. This is above their guidance of a net debt / ebitda between 3.0 and 3.5. Halfway 2025 they expect to be in the range of 3.0 – 3.5 again. This means as of that time most cash will be returned to shareholders in dividend or share buybacks.

With such a high number of debt we have to look at how this debt has been financed. Out of the 9.2B debt:

~0.5B in incremental term loan with variable fee (SOFR plus applicable rate) maturity date April 2024

~1.0B in senior notes 3,125% with maturity date September 2026

~1.5B in senior notes 5,00% with maturity date August 2027

~2.0B in senior notes 4,00% with maturity date July 2028

~1.2B in senior notes 5,50% with maturity date July 2029

~1.5B in senior notes 4,125% with maturity date July 2030

~1.5B in senior notes 3,875% with maturity date September 2031

Their 2023 Annual report says: “Under the Credit Facility, Sirius XM, our wholly owned subsidiary, must comply with a debt maintenance covenant that it cannot exceed a total leverage ratio, calculated as consolidated total debt to consolidated operating cash flow, of 5.0 to 1.0.”

According to S&P Global, the adjusted net leverage will increase to around 4x at transaction close, as SiriusXM will assume about 1.5B debt from LSXM.

“Despite the expected near-term increase in leverage, we view the simplified ownership structure as a credit positive. We expect the company to prioritize debt reduction and forecast leverage to decline to about 3.8x in 2024 and 3.3x in 2025. As a result, we placed our 'BB' issuer credit rating on Sirius XM on CreditWatch with positive implications.”

Currently Sirius XM is on a BB credit rating for their unsecured debt only. The companies senior secured debt is on BBB-issue-level rating. A potential upgrade after the merger will be limited to one notch. BBB rating means there is adequate capacity to meet the financial commitments.

“However, Sirius XM generates free operating cash flow (FOCF) of more than $1 billion annually, which supports deleveraging. While Sirius XM's dividend policy will remain unchanged (around $410 million expected in 2024), management has said that it expects to deemphasize share repurchases to focus on debt reduction. Management has publicly affirmed its leverage target of low- to mid-3x and expects to reduce leverage back to this level between the middle and end of 2025.”

Source: S&P Global

The new company will be a company with high debt, although they will be back to a leverage of 3.3 by the end of 2025. This is the range where the company wants to be. The interest expenses for 2023 came in at $423M and for 2024 I forecast this at $440M. If I assume they will repay the 2026 loan in 2025 to reduce their debt with $1B and they will refinance their 2027 loan against 6%, then their interest expense will be back at $425M in 2025.

Let’s start with the valuation. I will use the forecasted revenue budgeted by management for 2024 and 2025 and will increase revenue and costs by 2% due to inflation. Hence expecting flat revenue, as the upward trend in revenue was broken last year and I would like to see a conservative case.

I also calculate with an EBIT margin of 20.8% and a WACC of 8.63%. Using the DCF-method I come to an enterprise value of $22.8B, but I have to deduct the net debt of $9.5B, so the Equity value is $13.3B. With 3,387 shares outstanding this is $3.92 a share. If I multiply this with the ratio of 8.4 I come to a fair value of $ 32.93 for the LXSM shares, while current share price for e.g. LSXMA is $24.31. That is a discount of 35%. In this conservative model I assumed share buybacks will start again in 2026 and will continue in 2027 and 2028. Considering these buybacks, a flat revenue and an increasing interest expense and using a P/E of 12.8 I get to a yearly return till the end of 2028 of 15,0% (including dividends). That seems attractive.

The 10-year Growth CAGR for Revenue has been 8,95%. I just want to understand what would happen if this growth would continue. If I would take the expected revenue given by management for 2024 and 2025 and the historical growth of 8,95% for 2026 – 2028, then instead coming of $3.92 a share I get to a value of $ 5.74 or $48.21 for LSXM shares. This would mean a discount to fair value of 98%.

The new P/E would come to 18,7 I would get to a potential share price end 2028 of $ 9.45 or a yearly return including dividends of 29%. I know competition is fierce and market currently doesn’t believe it, however Berskhire is buying agressively.

Risks

Substantial competition which is likely to increase. It’s a fierce competition on time and attention of listeners with other content providers, where some content is offered for free to listeners.

Competitors streaming products may be pre-loaded or integrated into consumer electronics products or vehicles.

Competition could result in lower subscription, advertising or other revenue and to an increase in expenses.

War in Ukraine: an expansion of the war in Ukraine to other countries, particularly Romania, could materially affect their ability to deliver advertisements on their Pandora services.

The number of subscribers to Sirius XM service declined in 2023 and may further decline in the future.

Agreements with automakers to include satellite radios in new vehicles could be impacted if automakers decide not to include Sirius XM services going forward.

Failure of satellites would significantly damage the business.

Source: Sirius XM Holding 10k filing 2023

Summary

Company with stable earnings and high free cash flow (yield of 12% increasing in 2025 to 15%).

Discount to fair value of 35% in the conservative case with strong potential upside.

Potential acquisition target.

High debt: guidance of a net debt / ebitda between 3,0 and 3,5 expected mid 2025.

Fierce competition, but strong core audience and long-term agreements with automakers.

I have bought LSXMA for my portfolio, as the margin of safety (35% discount) using a conservative case makes it an attractive buy with potentially more upside to come.

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.